Colocation in ERCOT Evolves, Virginia Fast Track, and More

Here's what happened in the past 2 weeks across policy, large load development, and the generation queues

Policy Watch

State PUC dockets don’t always get a lot of coverage, but they’re where some of the most consequential decisions on large-load interconnection, data center cost allocation, and co-location arrangements are being made right now. Luckily, GridTracker’s Model Context Protocol (MCP) connection allows us to search and surface relevant filings across state PUC dockets and FERC directly. So in addition to providing bi-weekly updates on generator interconnection queues, starting this edition we’ll be covering the proceedings we think are worth watching.

Texas PUCT

Crusoe/Goodnight Wind Co-location, Round Two (Docket No. 59220)

We mentioned this case in a previous newsletter (and it received some news coverage earlier this year as well). The Crusoe/Goodnight Wind co-location (Docket No. 58881) was effectively Texas’s first real test of SB6’s new co-location framework. It involved a 260 MW AI data center (developed by Crusoe, operated by Ensign), located behind a 265.5 MW wind farm in Armstrong County, sharing a single ERCOT POI. The PUCT approved this net metering arrangement with six conditions, the most contentious being a 30-minute mandatory curtailment requirement during grid emergencies.

The July 9th proposed order under Docket No. 59220 adds a second 260 MW data center at the same POI and settlement meter. ERCOT studied it and found no transmission security issues, and PUCT staff recommends approval under the same six conditions. The application also discloses that a second Goodnight Wind facility (260 MW) is planned at the same POI by May 2027, which would put two wind facilities and two data centers stacked behind a single interconnection point and shared meter. Crusoe and Ensign still object to certain aspects of the conditions, but they’re back for a second data center at the same site under the same requirements, which suggests the model is working even with the curtailment strings attached.

BTM Co-location and REC Accounting (Docket No. 59963)

MARA Holdings, who acquired Great Plains Wind, a 114 MW SPP wind farm in Gruver, Texas, is amending its Renewable Energy Credit (REC) Generator Certification to account for a co-located data center served as BTM load. Because the data center consumes generation before it reaches the POI meter, the existing REC certification no longer reflects the facility’s total renewable output, so MARA is amending it to allow self-reporting of total generation as the sum of what the meter sees plus what the BTM data center consumed.

This is a fairly minor REC accounting question, but it points to something that will come up in every renewable plus data center co-location arrangement: how to attribute and certify renewable generation when it is being consumed before it ever hits a meter.

Hyperscalers/Big Tech

Amazon Briefs for a Fast-Track Large-Load Queue in Virginia (Case No. PUR-2026-00011)

Virginia SCC is weighing whether to create a fast-track interconnection queue for large loads willing to self-fund infrastructure or commit to grid flexibility. Amazon filed its response on June 30th, arguing there are no legal impediments and asking the Commission to create a contractual framework for large loads to self-fund or self-build qualifying infrastructure in exchange for queue priority.

The brief points to Maryland’s recently enacted tiered interconnection priority legislation (Md. H.B. 1532), which gives large-load customers who commit to demand response and incremental resource investments top priority in load studies, as a working model. The SCC hasn’t ruled yet, but the filing is a signal that hyperscalers are willing to put money on the table and commit to flexibility if it means moving faster through the queue.

Microsoft Testifies on “Bring Your Own Power” in the APS Rate Case (Case No. E-01345A-25-0105)

This Arizona Public Service (APS) general rate case has drawn out some of the most direct testimony yet on how utilities should treat large data center customers. In the July 8th hearing, Microsoft’s expert witness was cross-examined on a “bring your own power” proposal Microsoft advanced as an alternative to APS building out additional capacity to serve data center load. Microsoft operates in APS’s territory as an Extra High Load Factor customer running near 100% capacity factor and testified that it is willing to pay its own interconnection costs and that those costs are not passed on to residential ratepayers. Western Resource Advocates pushed back, arguing that data center load growth is driving up electricity rates and delaying coal plant retirements. No order yet, but the record being built here on self-supply feasibility and the real resource planning costs of data center load is worth tracking.

In the News

PUCT, facing 438 GW of large-load requests (nearly 90% from data centers), approved rules for ERCOT to begin processing those requests in batches of 75 MW or larger on June 18th. The first cohort, called Batch Zero, will be studied together rather than project-by-project. The approach mirrors the cluster study model long used for generator interconnection. This is one of the more consequential structural changes to ERCOT’s large load interconnection process yet.

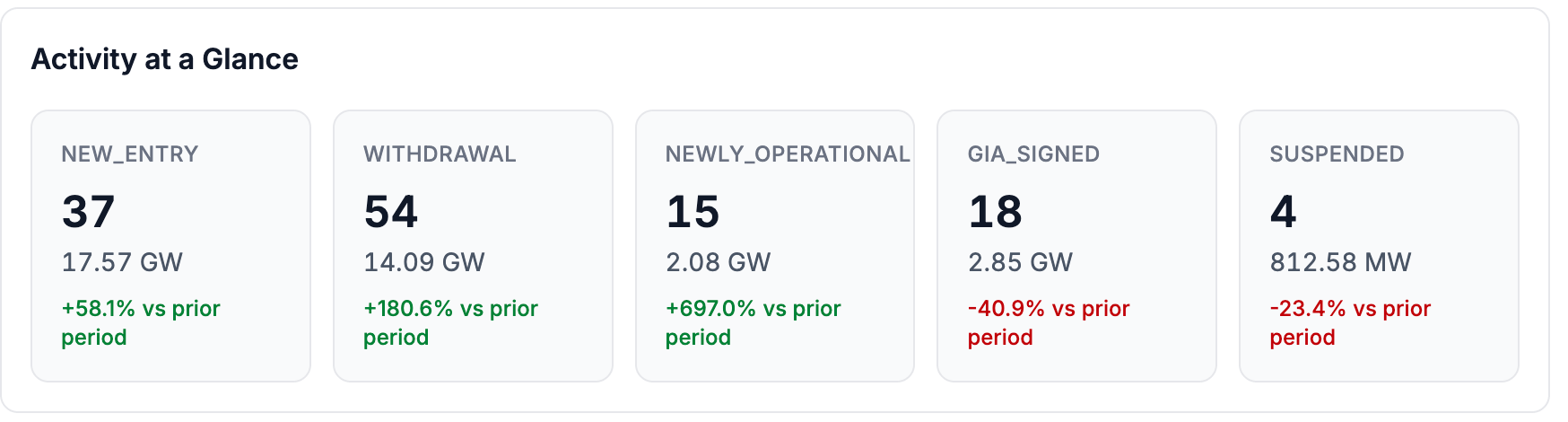

Queue Activity, June 27 - July 10, 2026

Additions: 17.57 GW (37 projects)

ERCOT: 14.05 GW, almost entirely gas, led by a cluster of large plants in central and east Texas.

MISO: 3.10 GW (7 projects), driven by gas and storage requests in Indiana and Louisiana.

Gas dominated new entries (~13 GW), followed by solar (~3.2 GW) and battery (~2.8 GW).

Withdrawals: 14.09 GW (54 projects)

CAISO: 7.44 GW of mostly Cluster 15 battery project exits.

ERCOT: 3.36 GW (16 projects), led by a 1.25 GW gas project withdrawal.

More than half of withdrawals were battery capacity (~7.5 GW), followed by hybrid solar+battery (~2 GW) and standalone solar (~1.7 GW).

Newly Operational: 2.08 GW (15 projects)

A very active period for projects reaching COD, up roughly 697% from the prior two weeks and concentrated in ERCOT (solar and battery).

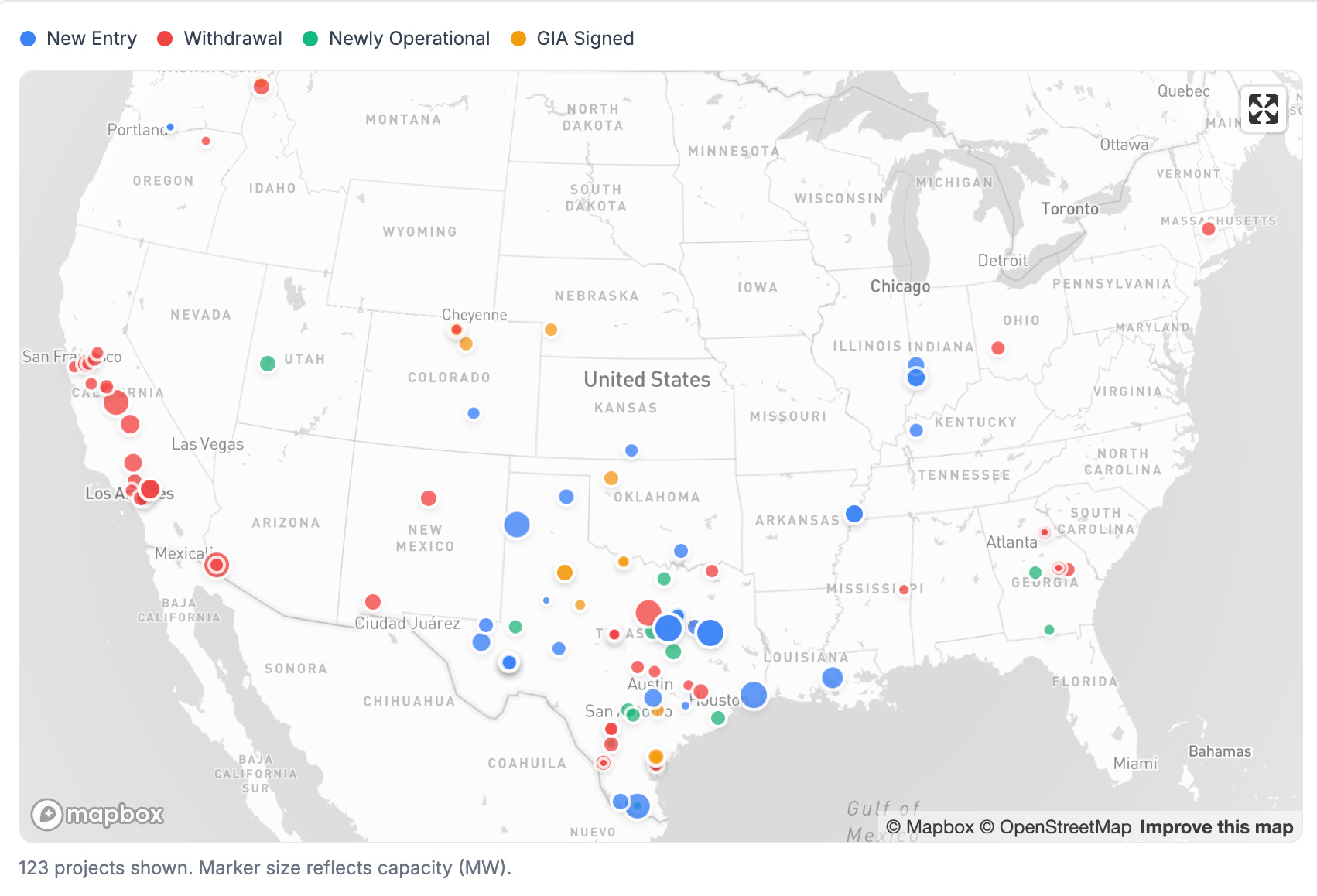

Activity Map

CAISO and ERCOT were both busy this period. ERCOT comprised the bulk of new entries (~14 GW of gas), GIA signings (solar, wind, and battery across central and east Texas), and projects coming online, while CAISO saw over 7 GW of Cluster 15 battery projects withdraw, concentrated in the Central Valley and the LA/San Bernardino area. MISO added roughly 3.1 GW of gas and storage in southern Indiana and Arkansas, offset by a single 1.54 GW Entergy Louisiana withdrawal. Elsewhere activity was comparatively light. A 300 MW battery project came online in Utah, a 250 MW gas project signed a GIA in northern Colorado, and scattered withdrawals registered in Oregon, New Mexico, and Georgia.

Queue Activity

Queue additions, withdrawals, and newly operational capacity were all sharply up from the prior two-week window. 17.57 GW of new capacity entered the queue across 37 projects, while 14.09 GW withdrew across 54 projects, a net addition of about 3.5 GW.

The entry side is almost entirely ERCOT, which accounted for 14.05 GW (roughly 80% of new entries, virtually all from gas) of new capacity entering the queues across the country. We are starting to see developer and project information in the queue data point explicitly to data center load both in ERCOT and, increasingly, in MISO. MISO added 3.1 GW across seven projects, some of which cited serving large commercial loads in their comments to the ISO.

CAISO saw 7.44 GW withdrawn this period, driven by Cluster 15 battery projects that had been in queue since the 2025 cluster cycle window. ERCOT had 3.36 GW in withdrawals, led by a single large gas project that had reached the facility study phase. 2.08 GW (15 projects) came online, up nearly sevenfold from the prior window. 2.85 GW across 18 projects signed GIAs, down about 41% from last period and were also ERCOT-heavy.

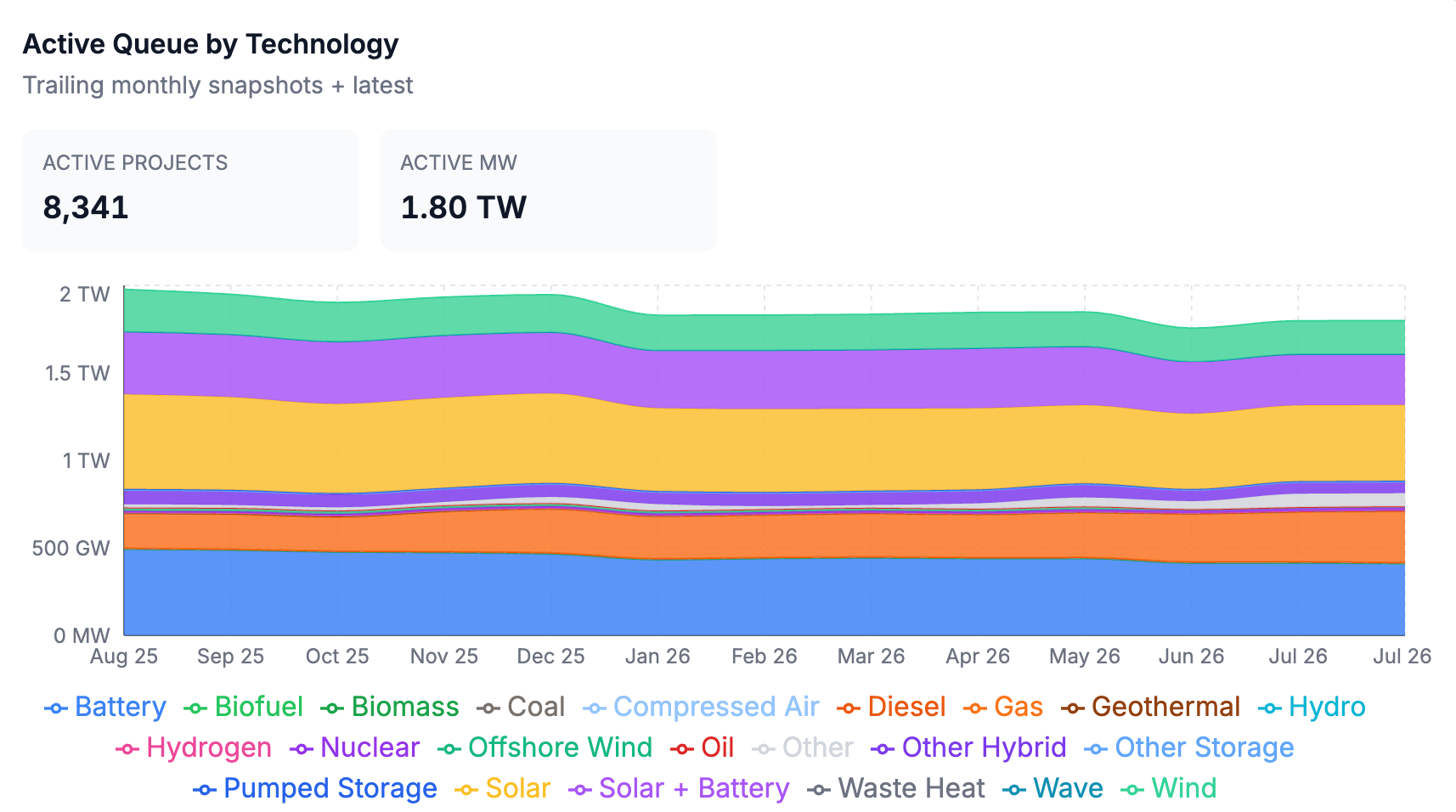

Queue Snapshot — Current State

The active queue stands at 1.80 TW across 8,341 projects, essentially flat from last period. The YoY composition shift towards gas and away from renewables continues. Gas is up 48%, nuclear 81.3%, and geothermal is up 171.1%. Against those gains, batteries are down 17.1%, solar down 19.9%, and wind and offshore wind are down 21.1% and 62.9%, respectively.

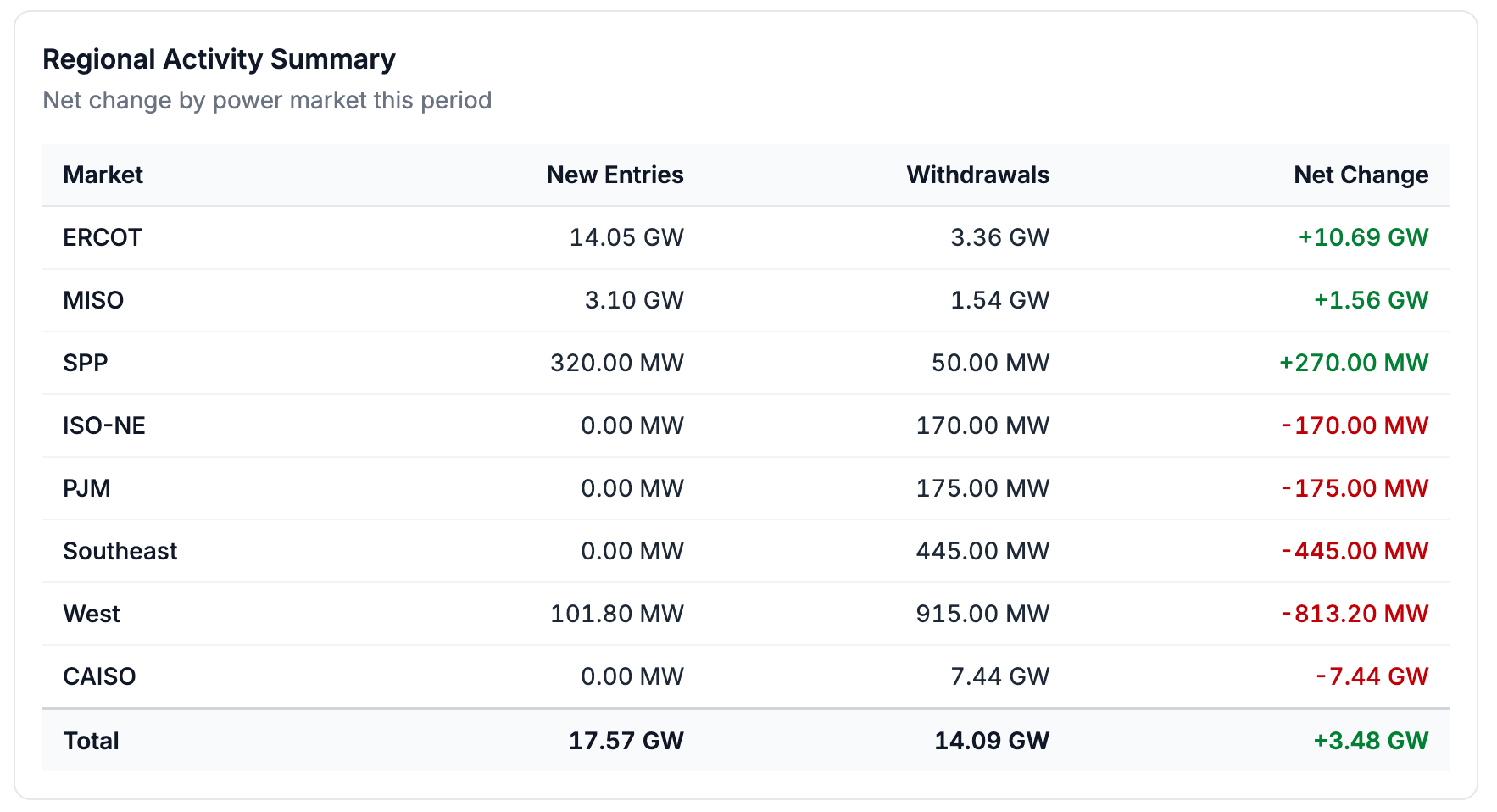

Regional Breakdown by ISO/RTO

On net, queues added +3.48 GW, with ERCOT as the sole major positive contributor at +10.69 GW. MISO added +1.56 GW on net; SPP edged up +270 MW. Every other market contracted: Southeast -445 MW, PJM -175 MW, ISO-NE -170 MW, the non-CAISO West -813 MW, and CAISO -7.44 GW.

Of CAISO’s 7.44 GW in withdrawals, roughly 67% (~5.0 GW) were standalone batteries, another 26% (~2.0 GW) were solar+battery hybrid projects, and the remaining ~6% (450 MW) was a single standalone solar project. Per CAISO’s published Cluster 15 (C15) Queue Report, project withdrawals for C15 started back in April 2025 and continued through earlier this month. C15 is one of the first clusters to move through CAISO’s reformed queue process. We be monitoring whether the projects that remain in C15 advance through study milestones and reach commercial operation at higher rates than projects from prior CAISO clusters.

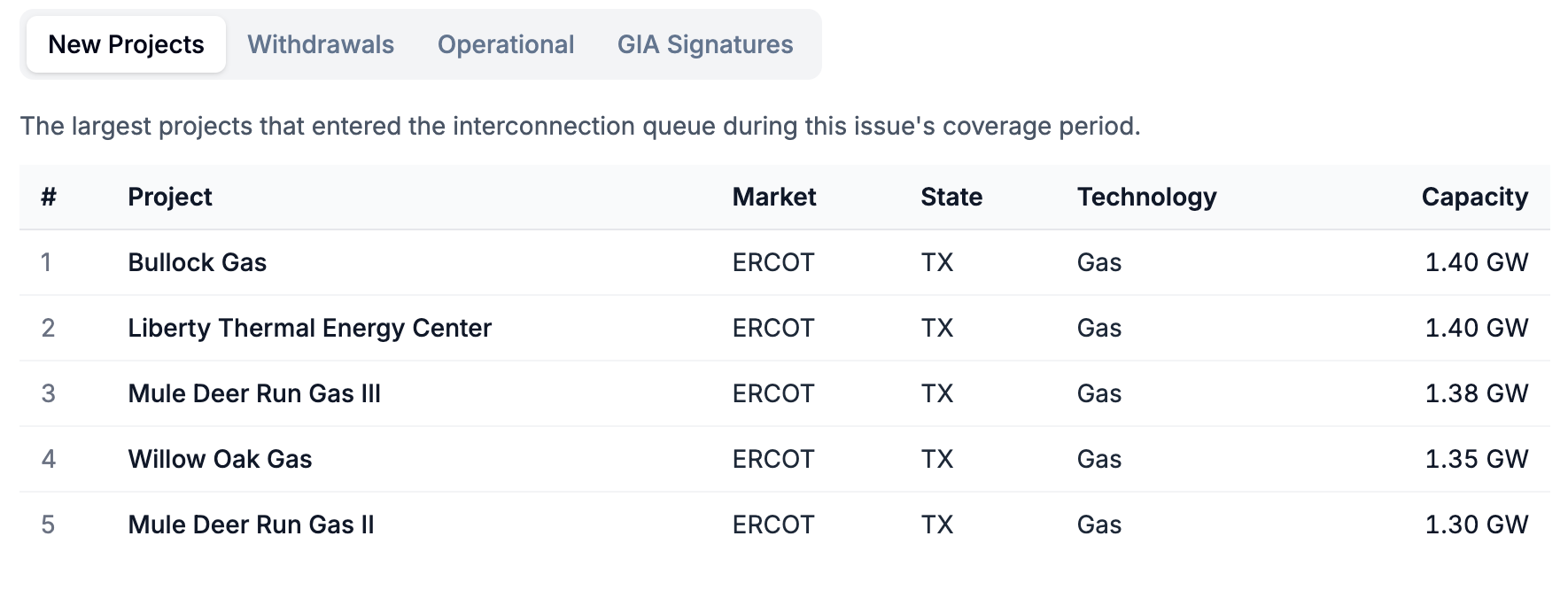

Notable Projects

ERCOT’s most recent queue data update confirms what has been widely covered in the energy space: lots of gas is being built in Texas, much of it to serve data center demand. The five largest projects added this period are all ERCOT gas plants. Developer/entity names like “Bullock Data Center, LLC” and “Liberty Data Center I, LLC” make the data center connection explicit in the queue record. Additions in MISO are telling a similar story, though on a smaller scale. Entergy Louisiana (Bayou Point Natural Gas, 750 MW), Duke Energy Indiana (Maple Creek Energy, 641.8 MW and Trotman Energy Center, 400 MW), and Entergy Arkansas (two projects, 400 MW each) all cited serving large commercial loads in the comments accompanying their queue requests.

The COD activity this period is worth quickly flagging. 2.08 GW came online, the most active two-week window of the year so far, and a reminder that a meaningful amount of capacity is actually crossing the finish line. The breakdown was roughly 44% solar, 33% battery, and 23% solar+battery hybrid, and 12 of the 15 projects that came online are in ERCOT.

Want to go deeper? GridTracker users get access to:

Project-level insights (see the project-level changes that occur in real-time)

Exportable datasets (export the full list of newly operational, withdrawn, GIA-signed, and added projects)

Interactive graphs and visualizations

Custom dashboards with real-time alerts and data export

Exclusive in-depth industry reports

… and much more!

| A guest post by

|

| A guest post by

|