Amazon Goes Nuclear in ERCOT, Virginia Weighs Overhaul to Transmission Funding, and More

Here's your roundup for the most important factors impacting the grid over the past two weeks

What happened from June 13 - June 26, 2026

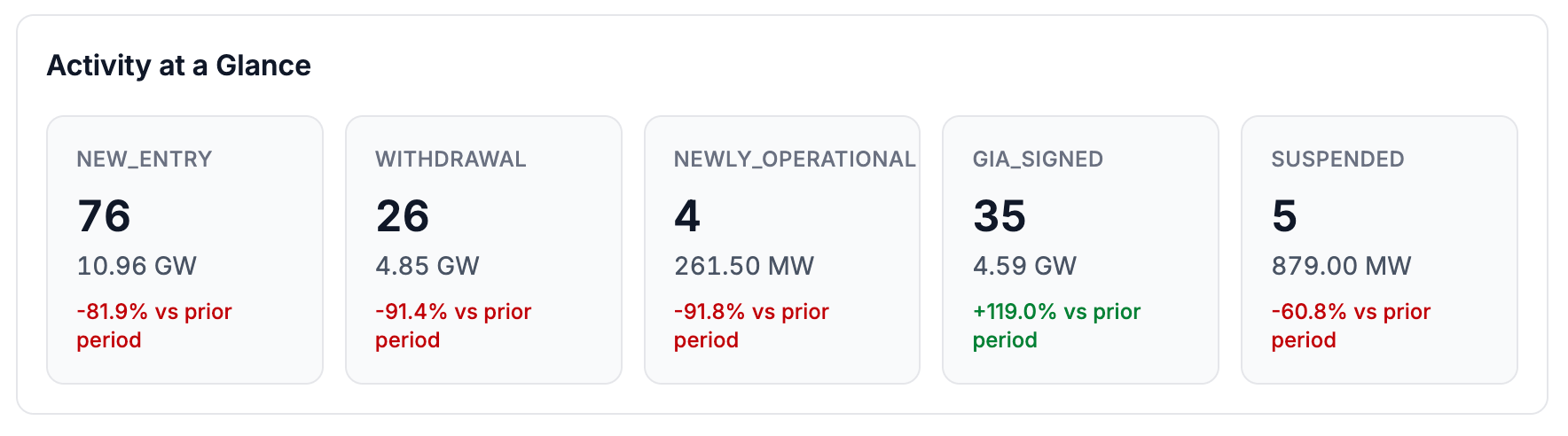

Additions: 10.96 GW (56 projects)

Non-CAISO West: 5.8 GW (20 projects), driven by Western Area Power Administration (WAPA) requests across Arizona, Nevada, and California.

MISO: 2.5 GW (6 projects), almost entirely a single unclassified tech type 2.2 GW Ameren Missouri request.

Southeast: 2.5 GW (29 projects), from Duke Energy Carolinas’ latest cluster.

By technology, gas led new requests (3.0 GW, 17 projects), followed by battery storage (2.4 GW).

Withdrawals: 4.85 GW (26 projects)

Withdrawals were spread across the West, MISO, and the Southeast.

West: 1.7 GW (5 projects), led by a 600 MW Idaho Power gas request.

MISO: 1.3 GW (9 projects).

Southeast: 0.9 GW (8 projects), split between Southern Company and Florida Power & Light.

CAISO: 0.4 GW (1 project), a single wind withdrawal.

In the News

FERC issues orders on large load interconnection. On June 18, FERC issued “Show Cause” orders to the six FERC-jurisdictional grid operators, requiring them to either demonstrate that their existing large load tariffs adequately serve large loads or revise them to address the issues the Commission identified. Each operator and its transmission owners have 60 days to respond, and within 30 days must file an informational report on how they will ensure adequate generation to serve existing and new large loads. The orders highlight five reform areas: more efficient transmission study and application processes; cost-shifting protections and cost transparency; accommodation of co-location and behind-the-meter generation; new transmission services for flexible large loads; and a process to study generation serving co-located and electrically proximate loads. The fifth reform area is one we will be watching as proposals come in, since study tracks for generation serving co-located load could create separate queue clusters/pathways to monitor and analyze.

Virginia weighs making large loads pay up front for the transmission they trigger. In a Dominion transmission rate case, Virginia State Corporation Commission staff filed testimony on June 16 recommending that the cost of transmission lines and upgrades built to serve a single high-load customer be assigned directly to that customer rather than spread across the rate base. Staff would do this by modifying Dominion’s line-extension policy to recover those facilities through Contribution-in-Aid-of-Construction, meaning the triggering customer pays up front. The recommendation builds on the Commission’s 2025 biennial order, which directed Dominion to develop alternative ways to allocate transmission costs. As the largest data-center market in the country, whatever Virginia codifies may become a reference point beyond PJM.

Amazon and Vistra take Texas co-location to a nuclear plant (Deep dive at the bottom of this issue). Comanche Peak Power Company and Amazon are seeking PUCT approval for a net metering arrangement that would place up to 1,200 MW of behind-the-meter data center load at the existing 2,400 MW Comanche Peak nuclear plant in Somervell County, under the same SB6 framework as the Crusoe-Goodnight case we covered last issue. The data center would install its own backup generation, sized to cover its full load and kept off the transmission grid, so that during an emergency the load runs on backup. The applicants go further, committing to making all of Comanche Peak’s capacity available to Security Constrained Economic Dispatch within 30 minutes of an ERCOT instruction. It is a notable contrast with co-location cases elsewhere, where data center developers have resisted curtailment, and could be a sign of hyperscalers making efforts to trade grid-friendly terms for a faster path online. More on this below.

Gas turbine shortage tests PJM’s fast-track rules. Advanced Power Services, developer of the Chestnut Run gas project in Ohio, has asked FERC for a waiver to swap in lower-output turbines after manufacturing backlogs pushed its in-service date out by at least two years. The swap would trim the plant’s maximum output but let it hold close to its original online date. The catch is that PJM’s Reliability Resource Initiative, the shovel-ready fast track, bars changes to a project’s size or Capacity Interconnection Rights, so the substitution needs a waiver. PJM protested on June 18, arguing the request fails FERC’s waiver criteria and would hand Advanced Power an unfair edge over developers complying with the tariff, and noted the company could instead use the Expedited Interconnection Track FERC approved on June 9.

Worth a Read

Coverage of, and commentary on, FERC’s large load interconnection order:

Jackson Ewing (Duke Univ.) in Latitude Media.

The case for auctioning interconnection and flexible large-load service from Chris Gillet.

An updated review of ISO/RTO generator interconnection processes from GridStrategies and Brattle Group.

The long-awaited 2026 edition of LBL’s Queued Up report is finally here! GridTracker was happy to serve as data providers in a fruitful partnership for this project.

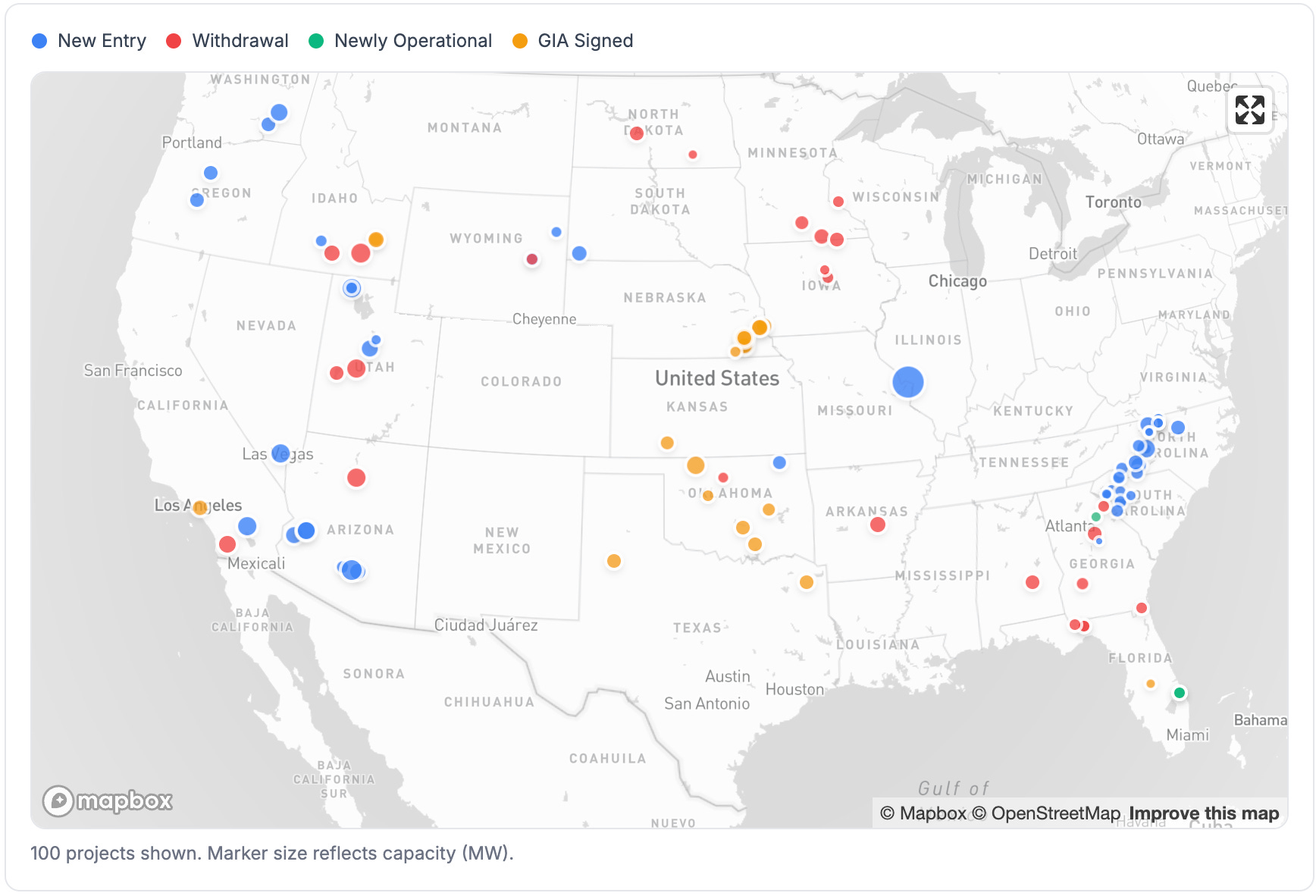

Activity Map

The main action this period is in the non-CAISO West and Southeast. New queue requests came in from the Southwest (WAPA), the Mountain/Pacific Northwest (Idaho Power, BPA, PacifiCorp, Black Hills Power), and a new cluster from Duke Energy Carolinas. Withdrawals were scattered, showing up across the Mountain West, the Upper Midwest in MISO, and the Southeast. There was also substantial GIA activity in SPP.

Queue Activity

This was a relatively quiet period for the queues, with additions, withdrawals, and newly operational activity all down from the prior period. The two-week totals come to just under 11 GW of new entries against 4.9 GW of withdrawals, a net addition of about 6 GW.

New entries were led by Duke Energy Carolinas, which added 28 projects totaling 2.5 GW across North and South Carolina, mostly battery storage (about 1.4 GW) and gas (roughly 0.7 GW). A WAPA Desert Southwest cluster of about 3.3 GW across eight projects in Arizona, Nevada, and California accounts for most of the West’s activity (a mix of gas, battery, and solar+storage). The single largest request is a 2.2 GW project from Ameren Missouri in MISO, which entered the queue seeking network resource service and sits in its application window. It has not yet been assigned a resource type in the MISO queue data, so it accounts for much of the “Other” capacity this period.

Withdrawals were broadly distributed, the largest being a 600 MW Idaho Power gas request and a 500 MW solar+storage project in SPP. Only four projects reached commercial operation this period, all small Florida and Georgia solar projects in the Southeast.

The standout metric this period is GIAs signed, up about 119%to 4.6 GW. Most of that is a cluster of Nebraska public-power gas units, from NPPD and OPPD, reaching interconnection agreements in SPP.

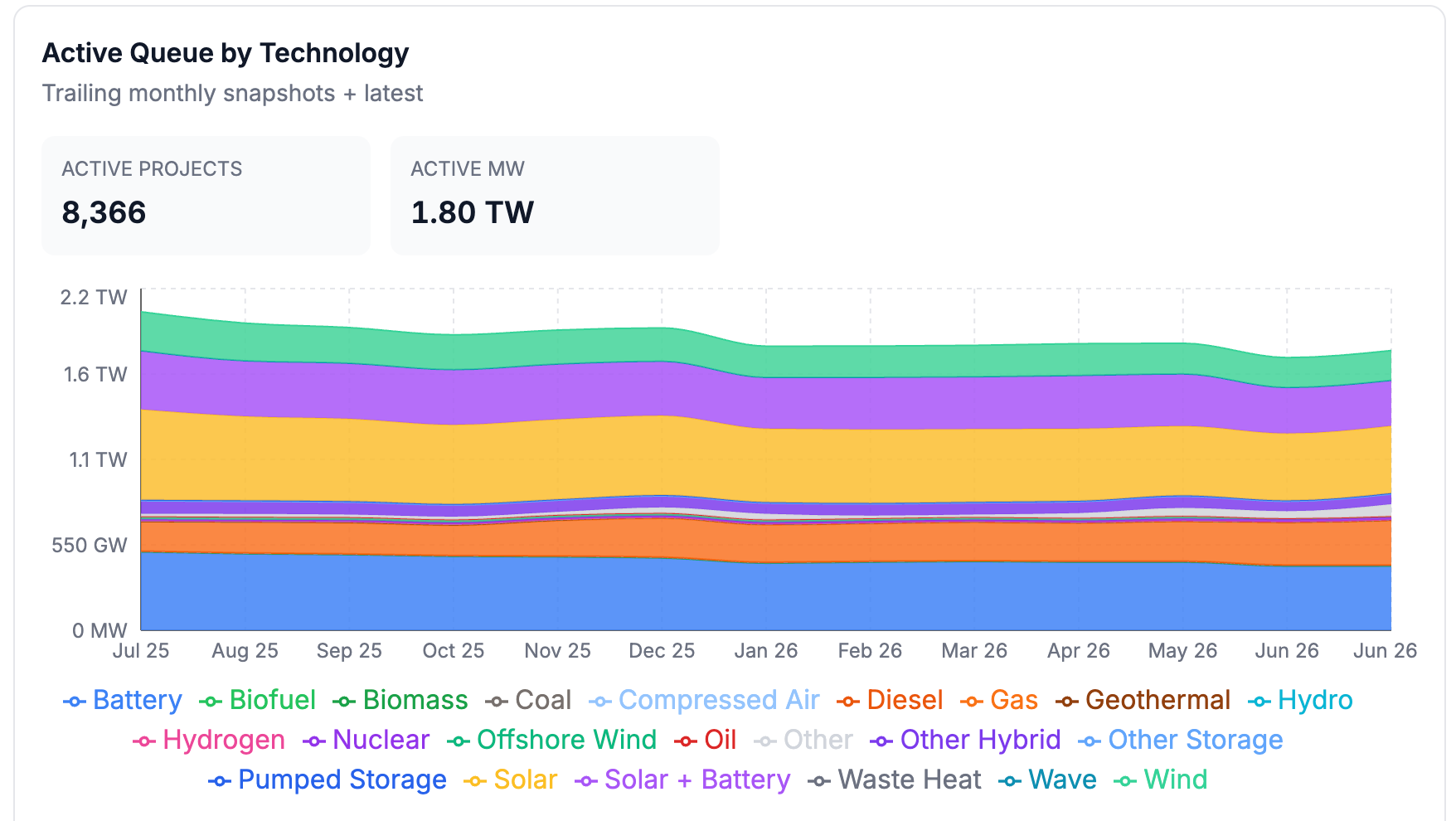

Queue Snapshot - Current State

The active queue stands at 1.80 TW across 8,366 projects, and is still overwhelmingly solar and battery by volume. Firm resources continue to gain share even after a relatively quiet couple of weeks for the queues, with gas up about 51 percent, nuclear up 81 percent, and geothermal up over 170 percent year-over-year, while battery, solar, and wind are each down by double digits. As we have noted before, the outsized swing in "Other" (up roughly 349 percent) is mostly unclassified new entries like this period's Ameren (MISO) request that have not yet been assigned a technology, so it overstates how much genuinely uncategorized capacity is entering the queue.

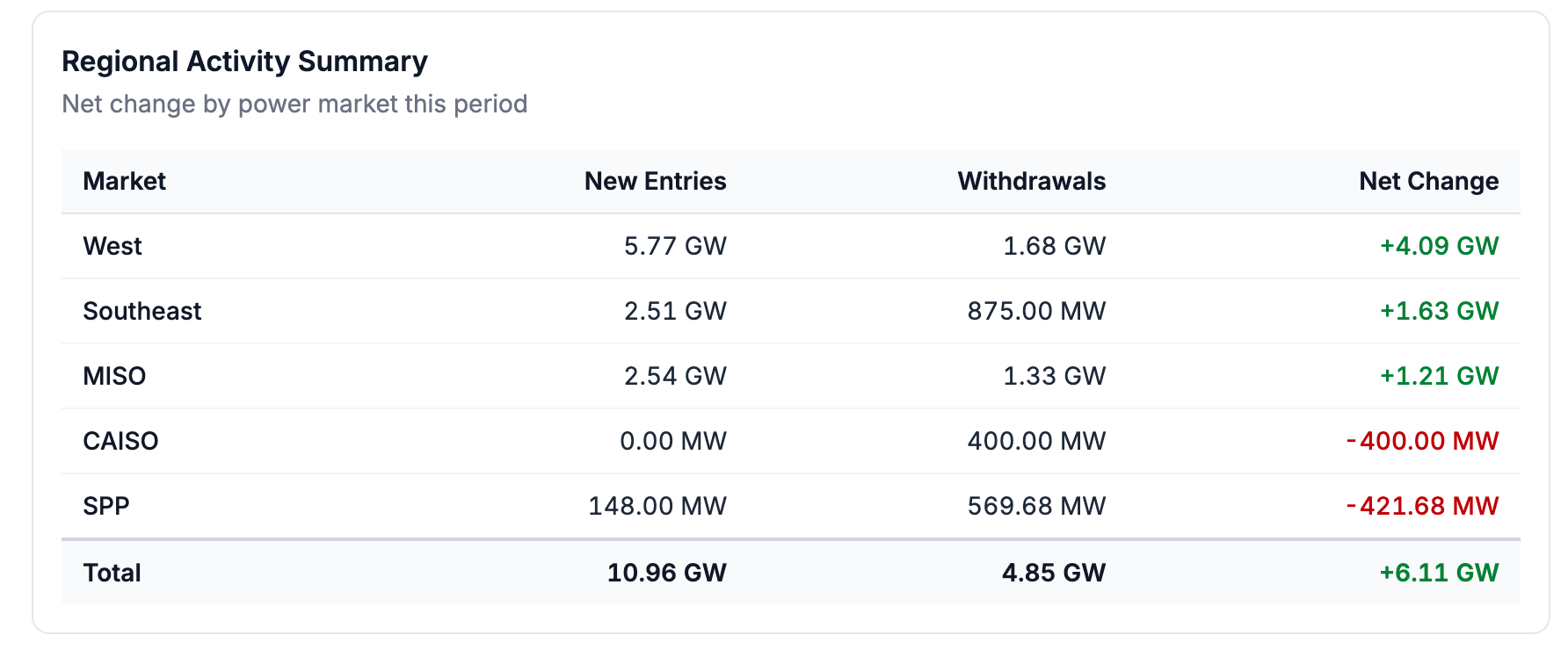

On net, the queue grew by about 6.1 GW this period.The non-CAISO West leads at +4.1 GW on the WAPA cluster, followed by the Southeast at +1.6 GW on Duke's Carolinas additions and MISO at +1.2 GW. Only two markets contracted, both marginally: CAISO at -400 MW on a single wind withdrawal and SPP at -422 MW. PJM, which dominated last period's withdrawals as it cleared its legacy serial queue, is quiet this time, with the reformed cluster process queue data still pending release.

Amazon vs Crusoe: A Test of Two Distinct ERCOT Co-location Strategies

We’ve recently covered two contrasting data center architectures for co-location in ERCOT.

On one hand, we have Crusoe: they are proposing to co-locate two large data center facilities, Crusoe One (265.5 MW) and Crusoe Two (260 MW), behind a single existing wind farm (the 265.5 MW GOODNIT1), with a second wind farm (GOODNIT2, expected commercial operation May 2027) planned to be added behind the same point of interconnection later.

Under ERCOT’s proposal, both Crusoe facilities would need to fully curtail (525.5 MW of firm AI load combined) in exchange for taking a 265.5 MW intermittent wind generator into the net metering arrangement. That’s a 2:1 ratio between curtailed firm load and removed intermittent generation.

It’s important to note the Crusoe facilities are co-located with intermittent wind power. This means these facilities cannot remain fully behind-the-meter. They regularly need to draw power from the ERCOT grid when wind output is below the facility’s demand. Secondly, based on testimony in this PUCT filing, they do not appear to have full backup generation readily deployable. We are inferring this from the harm argument in that testimony, where Crusoe’s expert argued the following about a 30-minute shutdown window:

“Abrupt, unplanned curtailment carries serious operational risks: cascading hardware failures across server clusters, corruption or loss of active computational work that cannot be recovered, data storage integrity failures, and thermal events caused by the sudden loss of coordinated cooling infrastructure. These are not hypothetical concerns - they are documented in this record.”

— Bojorquez Testimony, PUCT Docket 59220, Item 21, June 3, 2026

That does not paint a picture of a facility which has full, rapidly available backup generation on-site.

We contrast this against Amazon’s Comanche Peak filing (PUCT Docket 59399), widely reported as “Project Spectrum.” This is a recent proposal to co-locate a data center of up to 1.2 GW behind an existing 2.4 GW nuclear plant (Comanche Peak). This facility is planned to be fully behind the meter, with the load not expected to ever be served by grid power (per Amazon’s application in the docket). Also crucially, Amazon explicitly plans to establish sufficient backup generation on-site, sized “equal to or exceeding” the load’s expected demand, to power the entirety of their facility. For this reason, Amazon is preemptively offering the 30-minute mechanism directly in their application, rather than waiting to negotiate around ERCOT’s proposed conditions. However, their architecture grants them a convenient luxury which Crusoe seemingly does not share: they structure the guarantee as a return of Comanche Peak’s full capacity back to the grid, and not a shutdown of their facility. In the case of such an event, Amazon plans to simply switch to their fleet of on-site backup generators. Based on the testimony filed by Crusoe’s expert and referenced above, it appears that Crusoe does not expect to have this same capability.

It’s worth noting that under ERCOT’s proposed conditions, the backup gen must be sized to serve the full facility load, and not just enough to offset what the co-located generator was contributing behind the meter. So a developer co-locating a 1 GW facility with a 50 MW generator would need to build roughly 1 GW of backup, not 50 MW, if they want to remain operational through a grid emergency. The sizing requirement scales with the data center, and not with the co-located generator.

And here we see the pattern that’s likely to emerge in ERCOT for future co-located projects: full backup power is likely to become an absolute necessity under the SB 6 framework. For facilities like Amazon’s with extremely high availability SLAs, full backup power was probably always a baseline requirement. So this precedent seems unlikely to dissuade those projects. The precedent from Docket 58881 (Crusoe One) and Docket 58872 (Freestone) already points in this direction. Docket 59220 (Crusoe Two) will determine whether that precedent solidifies or whether the Commission narrows the scope in response to Ensign’s proportionality argument.

Want to go deeper? GridTracker users get access to:

Project-level insights (see the project-level changes that occur in real-time)

Exportable datasets (export the full list of newly operational, withdrawn, GIA-signed, and added projects)

Interactive graphs and visualizations

Custom dashboards with real-time alerts and data export

Exclusive in-depth industry reports

… and much more!